![]()

Medical Electronics Market to Surge from USD 12.78 Billion in 2026 to USD 23.80 Billion by 2035—Powered by FDA Cybersecurity Pre-Market Mandates

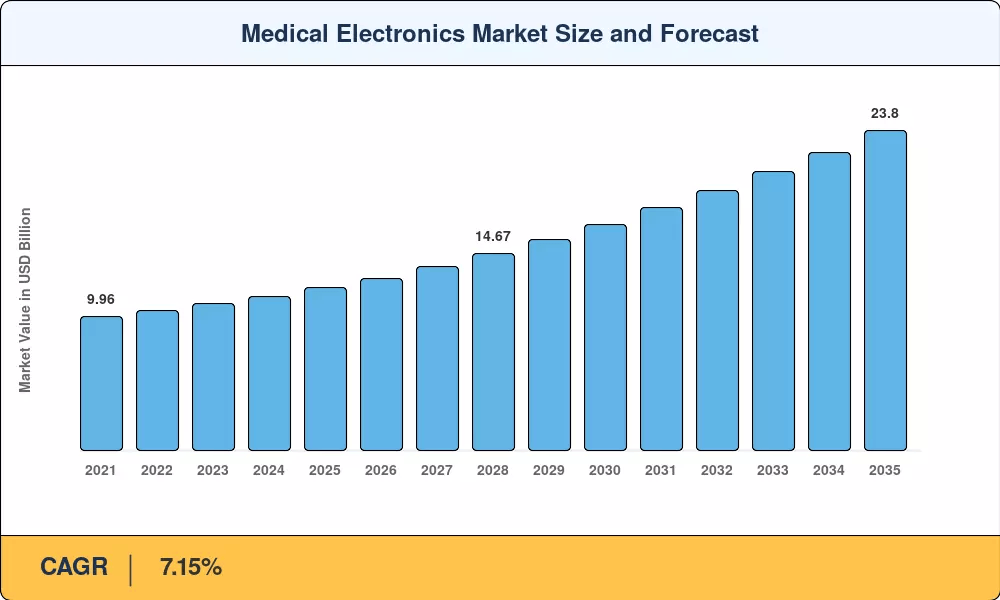

NY, CA, UNITED STATES, June 19, 2026 /EINPresswire.com/ — As per Market Research Future, the global Medical Electronics Market size to reach USD 23.80 Billion by 2035 from USD 12.78 Billion in 2026, at a CAGR of 7.15% during the forecast period 2026–2035. The market base was estimated at USD 12.10 Billion in 2025.

The 7.15% CAGR—anchored by structural healthcare digitization demand rather than discretionary healthcare spending—is driven by three converging forces: the FDA’s 2024 cybersecurity guidance that compels OEMs to redesign connected devices with embedded software bills of materials, sustained CMS value-based reimbursement migration that channels hospital budgets away from episodic imaging purchases and toward continuous-monitoring platforms, and AI/ML diagnostic integration that has converted medical electronics from standalone hardware into intelligent, inference-capable platforms.

National governments and multilateral health organizations are amplifying this momentum. The FDA had authorized over 1,450 AI/ML-enabled medical devices cumulatively by the end of 2025, with radiology accounting for approximately 76% of all cleared devices.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/40627

Key Market Trends & Growth Drivers

FDA Cybersecurity Pre-Market Mandates and Connected Device Proliferation

The FDA’s April 2024 final guidance on cybersecurity in medical devices mandates software bills of materials (SBOM) and coordinated vulnerability-disclosure processes for all connected devices submitted for premarket review. This policy shift compels OEMs to redesign connected devices with embedded SBOM documentation, threat modeling, and patch-management plans, adding 4–8 weeks and USD 80,000–150,000 to typical submission timelines.

The global wearable health technology market is experiencing sustained expansion, with billions of units currently active. Every new variant or software update for these connected devices must undergo stringent biocompatibility, electrical safety, and human-factors validation before market entry, driving demand for specialized third-party medical electronics validation services.

CMS Value-Based Reimbursement Migration and RPM Expansion

CMS Alternative Payment Models now cover more than 40% of traditional Medicare beneficiaries, channeling hospital budgets away from episodic imaging purchases and toward continuous-monitoring platforms that document outcome improvements.

This shift is especially visible in cardiology and pulmonology departments, where real-time telemetry data satisfies quality-measure reporting requirements. The medical electronics market benefits directly, as procurement committees increasingly evaluate total cost of ownership—inclusive of analytics subscriptions—rather than upfront hardware price alone.

AI/ML Diagnostic Integration and Edge-AI System-on-Chip Proliferation

Legacy analog instrumentation is gradually being replaced by digitally integrated systems, using edge-computing modules coupled with cloud analytics. The FDA had authorized over 1,450 AI/ML-enabled medical devices cumulatively by the end of 2025, with radiology accounting for approximately 76% of all cleared devices.

OEMs are now embedding inference engines directly into the GPUs of imaging systems, making AI-driven triage a standard expectation for new flagship CT and MRI platforms. This integration is effectively driving a premium on flagship hardware prices, as providers look to optimize diagnostic workflows.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/40627

Market Segment Insights

BY PRODUCT TYPE

Diagnostic Imaging: Dominant segment with ~42.5% revenue share in 2025. Reflecting sustained hospital capital expenditure on CT and MRI upgrades. Diagnostic imaging retains the largest product-type share, supported by a global installed base of CT, MRI, and ultrasound systems that demand periodic upgrades. Low-cryogen MRI is the highest-growth sub-category within imaging, as helium supply constraints push hospitals toward next-generation magnet technology.

Wearables and Implantables: Fastest-growing product type at 11.52% CAGR (2026–2035). Driven by RPM adoption and AI-enabled biosensors. Wearables and implantables represent the fastest-expanding segment: AI-enabled biosensors, continuous glucose monitors, and subcutaneous cardiac monitors are transitioning from niche clinical trials to mainstream reimbursement pathways, attracting significant venture-capital inflows.

BY COMPONENT

Sensors and MEMS: Dominant segment with ~34.6% revenue share in 2025. Reflecting miniaturization and multi-analyte integration across virtually every product category. Sensors and MEMS dominate component-level spending because virtually every product category—from imaging detectors to wearable patches—relies on transducer and signal-conditioning elements.

Power Management ICs: Fastest-growing component segment at 7.85% CAGR (2026–2035). Battery-life demands in wearable platforms drive demand for ultra-low quiescent-current designs. Power ICs are gaining strategic importance as OEMs extend battery run-times in ambulatory devices from 24 hours toward 14-day wear cycles.

BY END USER

Hospitals and Clinics: Dominant segment with ~47.9% revenue share in 2025. Installed-base refresh and IT-network integration dominate volume. Hospitals and clinics remain the primary revenue channel, purchasing integrated monitoring networks, imaging suites, and laboratory automation lines.

Home Healthcare: Fastest-growing end-user segment at 9.68% CAGR (2026–2035). Chronic-disease RPM reimbursement codes drive demand. Home healthcare is closing the gap rapidly as CMS, NHS, and other payers expand RPM reimbursement.

BY APPLICATION

Cardiology: Dominant application with ~31.6% revenue share in 2025. AF screening mandates and implantable monitor growth anchor this segment. Cardiology is the largest clinical-application segment, driven by the growing burden of atrial fibrillation screening programs and expanded indications for insertable cardiac monitors.

Oncology: Fastest-growing application at 11.10% CAGR (2026–2035). Liquid-biopsy hardware and image-guided therapy drive demand. Oncology is the fastest-growing application, propelled by convergence between imaging, molecular diagnostics, and AI-guided radiotherapy planning systems.

BY CONNECTIVITY

Wired (LAN / Field-Bus): Dominant segment with ~54.9% revenue share in 2025. Installed-base inertia in acute-care settings favors deterministic, low-latency links.

Bluetooth Low Energy: Fastest-growing connectivity segment at 8.84% CAGR (2026–2035). Wearable-to-gateway pairing proliferation drives demand. BLE 5.4’s channel-sounding feature improves ranging accuracy, enabling room-level patient localization alongside physiological data transfer.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/medical-electronics-market-40627

Regional Outlook

North America — Dominant Market (~35.8% Share, 2025)

The United States generates approximately 78.5% of North American Medical Electronics Market revenue, driven by CMS RPM reimbursement expansion, high per capita spending on devices, and developed hospital IT infrastructure—a single policy ecosystem that converted an analog-instrumentation-dominated market into one with a structural digital-native and AI-integrated tail.

The US dominates through a combination of aggressive cybersecurity mandate adoption, rapid AI/ML device authorization growth, and value-based reimbursement models that reward continuous monitoring over episodic imaging.

Europe — Second Largest (~27.4% Share, 2025)

Europe’s Medical Electronics Market reflects divergent national strategies—Germany leads regionally with Hospital Future Act digital-investment subsidies at 6.34% CAGR, while the UK historically used selective imaging targeting before broadening coverage through NHS diagnostic-hub expansion at USD 0.58 Billion in 2025.

France contributes ~15.4% of regional share through Ma Santé 2022 digital-health roadmap. Italy contributes ~11.2% of regional share on PNRR healthcare digitization funding. Spain contributes ~8.9% of regional share on National AI-health strategy. The Nordic countries hold ~7.3% of regional share on cross-border eHealth infrastructure.

Asia-Pacific — Fastest-Growing Region (8.62% CAGR, 2026–2035)

Asia-Pacific is the engine of the Medical Electronics Market. China holds the largest regional share with ~36.2% of regional revenue, driven by 14th Five-Year Plan hospital upgrades—significant capital has been effectively deployed to upgrade county-level hospitals and laboratory automation, sustaining strong demand for networked diagnostic and monitoring equipment.

India is growing at 10.12% CAGR on the back of Ayushman Bharat Digital Mission, with over 100 crore (1 billion) health records linked to Ayushman Bharat Health Accounts as of May 2026. Japan contributes USD 0.54 Billion through Society 5.0 health-tech adoption at steady pace. South Korea holds ~9.6% of regional share on K-Bio investment initiative.

Middle East & Africa — Emerging Opportunity (USD 0.74 Billion, 2025)

The Middle East & Africa carries the widest infrastructure gap and therefore the steepest opportunity. Saudi Arabia leads the region with Vision 2030 mega-hospital projects, contributing ~28.7% of regional share—the program includes five new mega-hospital campuses and the digitization of over 2,300 primary-care centers, creating a concentrated procurement wave for the medical electronics market in the Gulf.

The UAE contributes ~24.1% of regional share on Abu Dhabi Health Services’ smart-hospital plan. South Africa holds ~18.5% of regional share on National Health Insurance rollout.

South America — Growing Presence (USD 0.74 Billion, 2025)

Brazil anchors South America’s Medical Electronics Market at ~56.4% of regional revenue, with the Unified Health System investing in connected imaging and patient-monitoring networks across over 5,500 public hospitals, representing the largest single procurement program in South America’s medical electronics market and providing a stable demand floor that smooths regional forecasts. Argentina contributes ~21.3% of regional share on telemedicine regulatory framework formalizing reimbursement for remote diagnostics.

Competitive Landscape and Recent Developments

The Medical Electronics Market is predicted to be moderately to low concentrated, with an HHI of less than 1,000 and the top five firms together accounting for around 38–44% of global revenue. The competitive landscape is fragmented across diagnostic-imaging OEMs, semiconductor suppliers and specialist wearable-device firms. Competitive dynamics are multi-layered, and vertical integration is becoming a differentiator between leaders and followers.

The competitive landscape is stratified between broadest imaging portfolio leaders serving global hospital networks, strong home-health and RPM ecosystem providers capturing connected-care tenders, and component-level design-win dominance specialists consolidating the semiconductor supply segment.

KEY COMPANIES AND RECENT MILESTONES

GE HealthCare (2024–2025): Maintains leadership with CT, MRI, ultrasound and patient monitoring, commanding ~8–11% of global Medical Electronics Market revenue. Broadest imaging portfolio with Edison AI platform serves global hospital networks. Premium platform positioning in diagnostic imaging offsets tender-price compression in pooled procurement.

Siemens Healthineers (January 2025): Received FDA 510(k) clearance for an AI-powered photon-counting CT algorithm that reduces radiation dose by 45% while maintaining diagnostic image quality. Advanced imaging, laboratory diagnostics and digital health anchor a strong global franchise, holding ~8–10% of global revenue. The company benefits from the structural AI-diagnostic tail created by expanded imaging platform adoption.

Philips (November 2024): Announced a five-year strategic partnership with a major U.S. health system to deploy 15,000 connected patient monitors under an equipment-as-a-service contract valued at over USD 400 million. Patient monitoring, image-guided therapy, and connected care anchor a strong home-health and RPM ecosystem, holding ~7–9% of global revenue.

Future Outlook: 2026–2035

By 2030, ambient clinical intelligence and autonomous diagnostics will become the operating system of medical electronics. AI is shifting from simple decision-support overlays toward autonomous acquisition-and-interpretation loops. By 2030, an estimated 40% of routine chest X-rays in high-volume hospitals could be triaged entirely by FDA-cleared algorithms, significantly reducing the cognitive burden on radiologists for routine screenings.

Device manufacturers that embed “always-on” inference engines directly into hardware are increasingly positioning these capabilities as premium features, driving higher average selling prices across the medical electronics market. Digital twins enable predictive maintenance and virtual protocol optimization, cutting unplanned MRI downtime by up to 35% according to early RSNA pilot data.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/medical-devices-market-2869

https://www.marketresearchfuture.com/reports/wearable-medical-device-market-899

https://www.marketresearchfuture.com/reports/patient-monitoring-devices-market-2484

https://www.marketresearchfuture.com/reports/medical-sensors-market-2038

https://www.marketresearchfuture.com/reports/internet-of-things-in-healthcare-market-10671

https://www.marketresearchfuture.com/reports/digital-healthcare-market-7636

https://www.marketresearchfuture.com/reports/active-implantable-medical-devices-market-8834

https://www.marketresearchfuture.com/reports/medical-robotics-market-1311

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery